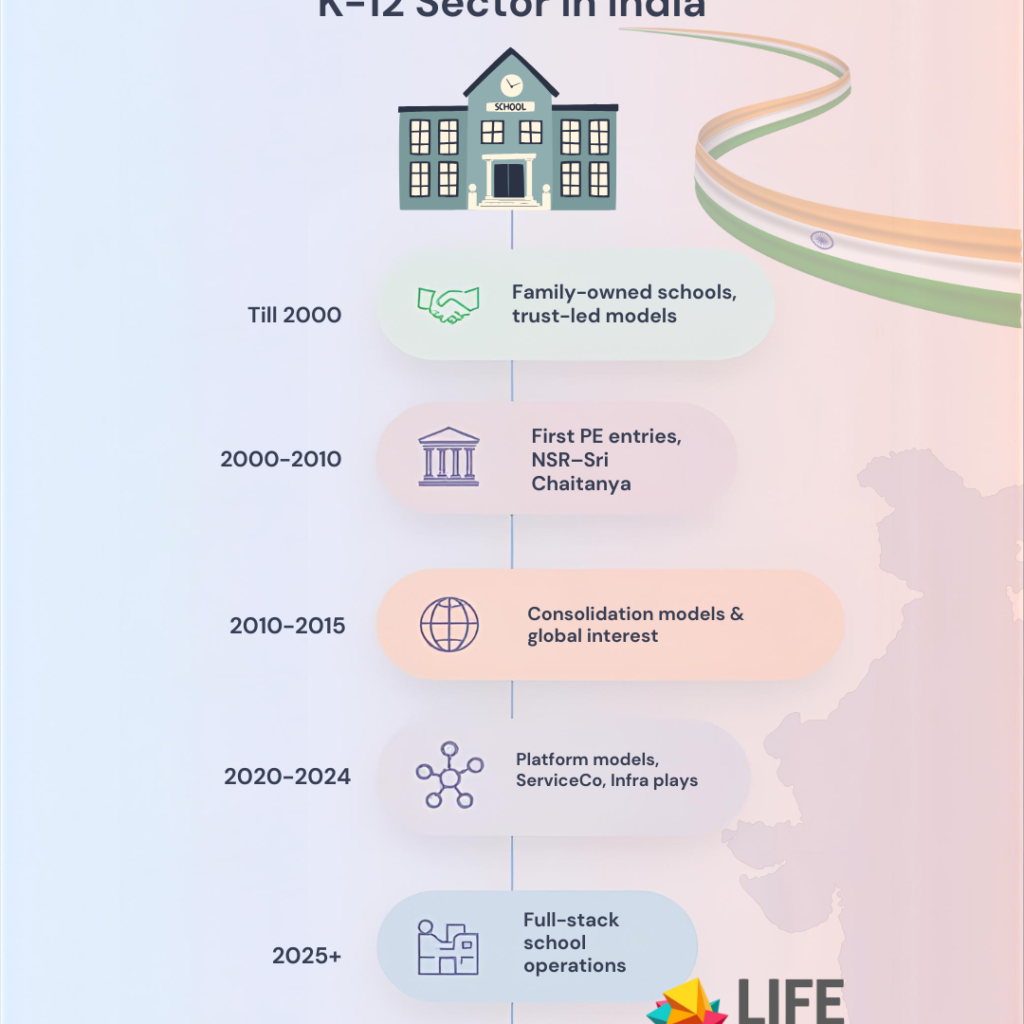

India’s K-12 education landscape is undergoing a historic transformation. Once a sector marked by family-owned institutions and passionate educator-founders, it has become a magnet for billions in private equity and venture capital.

This shift represents a fundamental reshaping of how schools operate, expand, and generate returns for investors—yet it carries profound challenges rooted in India’s unique regulatory framework and social mandate around education.

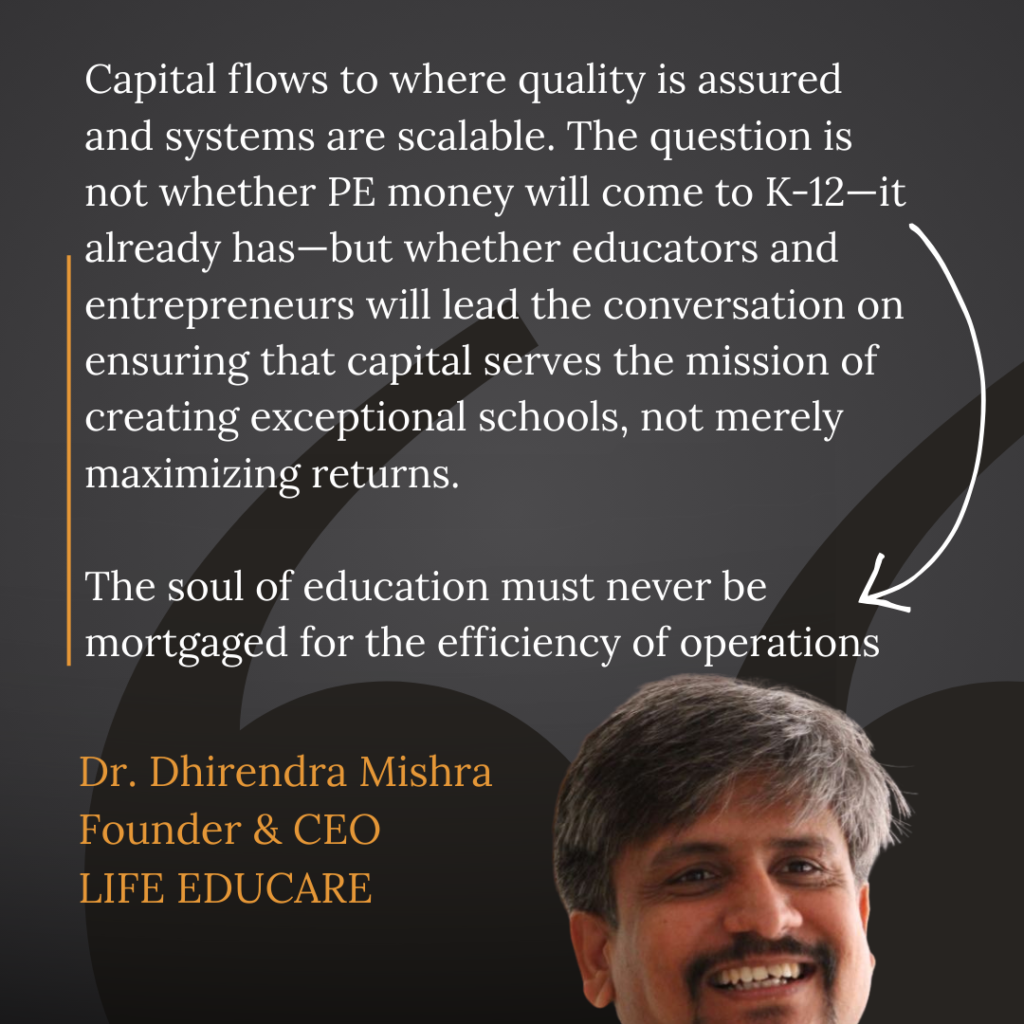

As Dr. Dhirendra Mishra, founder of LIFE Educare and a school startup and education management consultant of 70+ schools across India and gulf reflects on this phenomenon, “Capital flows to where quality is assured and systems are scalable.

The question is not whether PE money will come to K-12—it already has—but whether educators and entrepreneurs will lead the conversation on ensuring that capital serves the mission of creating exceptional schools, not merely maximizing returns.

The soul of education must never be mortgaged for the efficiency of operations.” This report serves as a comprehensive guide for entrepreneurs, investors, and stakeholders navigating this complex but high-potential ecosystem.

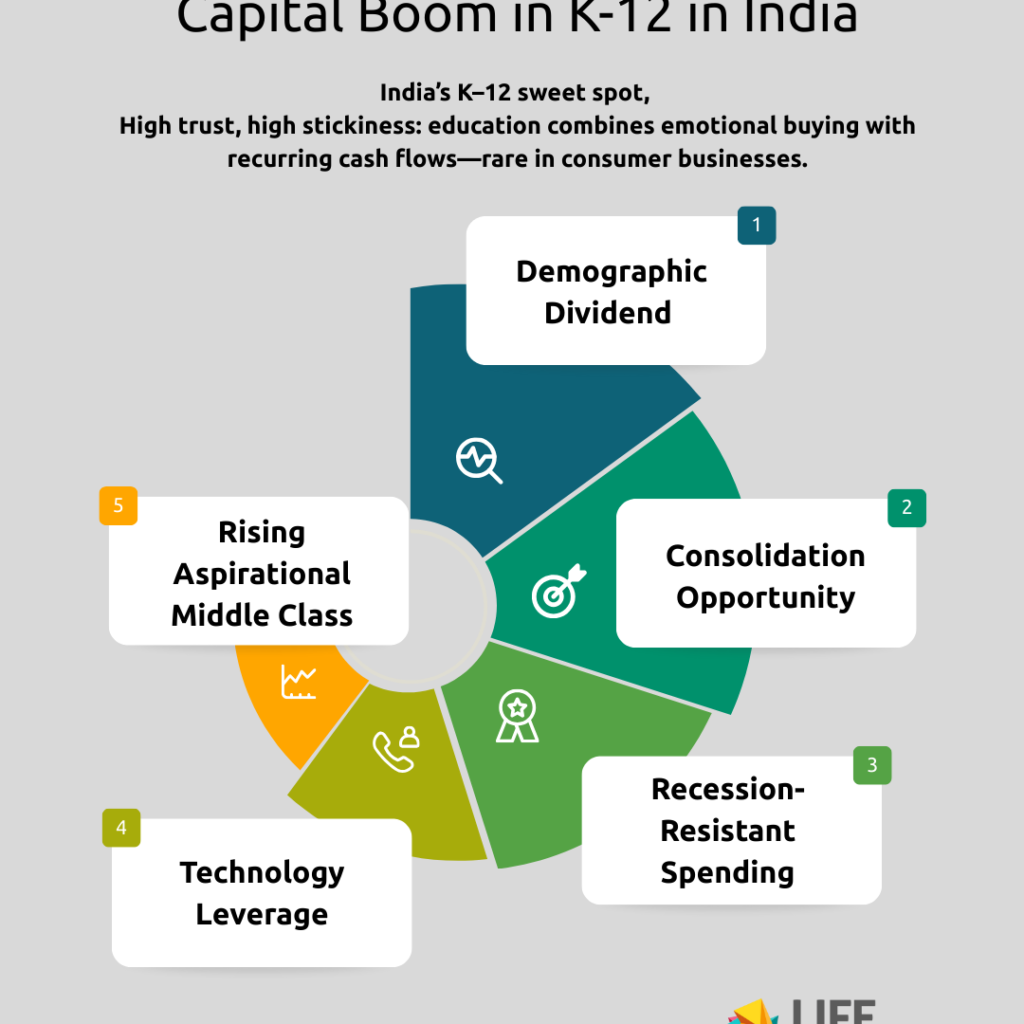

Market Fundamentals: Why PE is Betting on Indian K-12

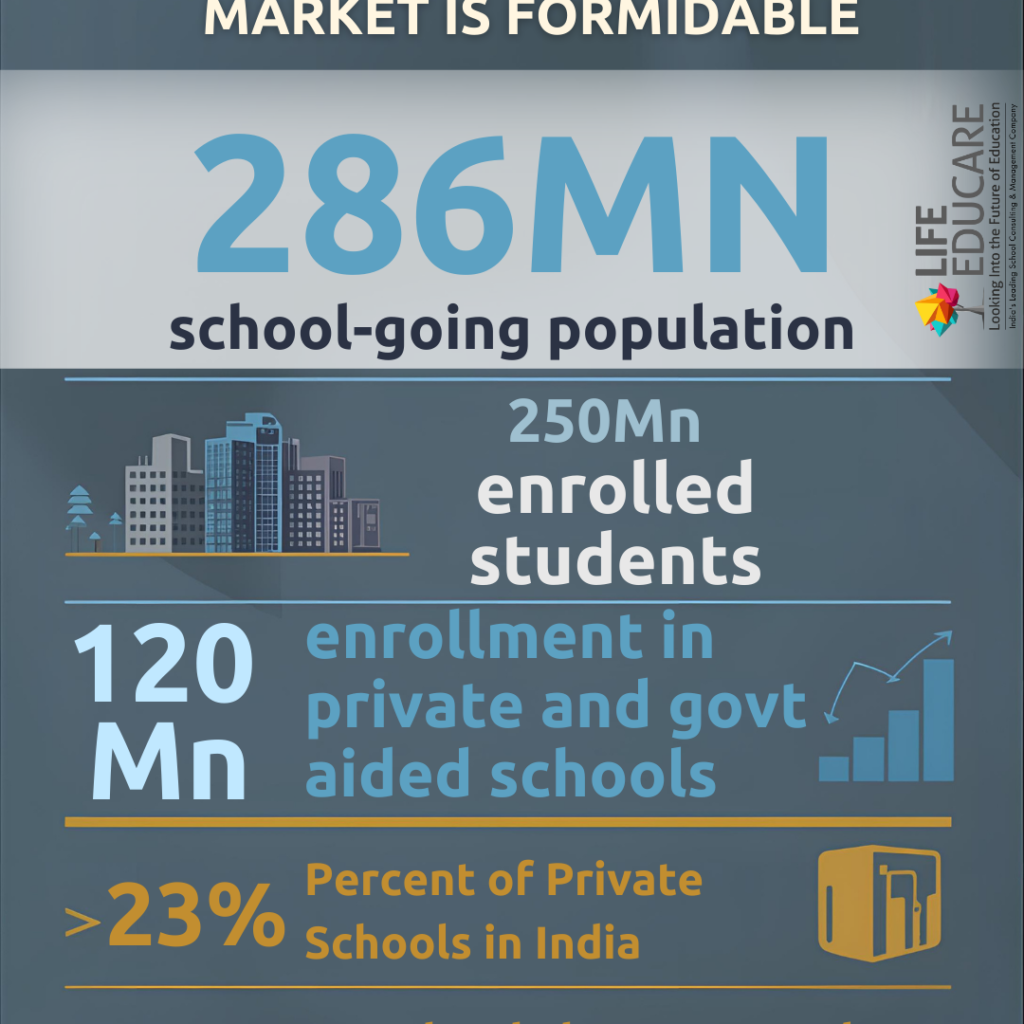

India’s K-12 education market is formidable: 375 million students, 260 million enrolled across 1.5 million schools, and private institutions capturing nearly half of all enrollments in major metros. Private K-12 transactions alone have exceeded $700 million since 2016, with institutional capital only accelerating. The thesis driving this investment is multifaceted.

- Demographic Dividend & Rising Aspirational Middle Class

- India’s upper-middle class and high-net-worth segments are expanding rapidly. Parents are willing to pay premium tuition for international curricula (IB, IGCSE), English-medium instruction, and holistic development—creating a pricing umbrella that supports sustainable margins.

- Consolidation Opportunity:

- The K-12 sector remains fragmented. While 1.5 million schools exist, the organized private school market is dominated by smaller regional chains. PE firms see an arbitrage opportunity: consolidate fragmented operators, apply standardized operational templates (curriculum, teacher training, procurement, technology), and unlock significant EBITDA expansion.

- Recession-Resistant Spending

- Education is largely insulated from cyclical downturns. Fee collection remains predictable, with recurring revenue streams that minimize customer acquisition costs relative to other consumer segments.

- Technology Leverage

- The integration of EdTech platforms (learning management systems, assessment tools, ERP for school administration) creates operational efficiency and improves unit economics. K-12 Techno Services’ model, for example, leverages a B2B SaaS approach through its Eduvate platform, servicing 800+ schools without owning them—a capital-light expansion that generates recurring revenue.

The PE Giants: Who’s Winning and How

KKR: The Flagship Play

KKR’s November 2019 acquisition of EuroKids (rebranded Lighthouse Learning) for ₹1,475 crore ($174 million) marked a watershed moment, signalling institutional confidence in the sector. Since then, Lighthouse has become the largest consolidated platform:

Network: 1,850+ pre-schools, 60+ K-12 schools, 190,000+ students daily

Brands under KKR

EuroKids, Kangaroo Kids, EuroSchool, Billabong High International, Centre Point, Heritage schools

Financial Trajectory

Revenue grew from ₹688 crore (FY23) to ₹1,000–1,200 crore (FY24), demonstrating the power of consolidation

In November 2025, KKR made a significant follow-on investment alongside Canada Pension Plan Investment Board’s PSP Investments, injecting approximately ₹1,760 crore ($200 million). This move signals KKR’s confidence in the platform’s ability to expand further while deepening its ownership and operational control.

PE Strategy

KKR’s approach emphasizes organic growth (adding 250+ pre-schools annually pre-2021, now 500+ annually) and disciplined M&A (acquiring Centre Point Schools in 2021). The firm is building a billion-dollar education services platform by leveraging shared infrastructure, standardized pedagogy, and technology systems across multiple brands—a “hub-and-spoke” model that competitors are now replicating.

Kedaara Capital: The Aggregator Play

Kedaara Capital’s investment in K-12 Techno Services represents the purest aggregator thesis in Indian K-12. K-12 Techno operates two distinct business models:

1. Orchids International Schools: Directly operated K-12 schools

2. Eduvate: B2B SaaS platform providing curriculum, content, and ERP to 800+ schools

Current Status (Dec 2024-Jan 2025)

– FY24 Revenue: ₹429.2 crore

– Students (Orchids): 54,493

– Operating Margins: 21.7% in 9M FY25 (vs. 15.6% prior year)

– Funding: $40 million from Kenro Capital (December 2024)

– Valuation: Sequentially rising from $420M (Sept 2023) to $540M (May 2024)

Kedaara is now in advanced discussions to raise $150–200 million at a $800–900 million valuation, with Vitruvian Partners (Europe), ChrysCapital, Warburg Pincus, and Permira reportedly competing. This validates the asset-light, high-leverage operational model where K-12’s capital expenditure is capped at security deposits and infrastructure investments rather than land acquisition.

Blackstone: Platform Building with Pace

Blackstone’s recent move signals a shift toward aggressive platform consolidation. The firm is in advanced talks to acquire a majority stake in Jayshree Periwal International School (JPIS) for $150–200 million, with plans to invest $600–700 million in building a consolidated education platform over the next few years.

Deal Structure: JPIS reported ₹135.2 crore operating revenue in FY25 with net profit doubling to ₹22.5 crore. Post-acquisition, existing management (founder Jayshree Periwal and CEO Ayush Periwal) will remain in place while Blackstone scales the platform across India. This mirrors Blackstone’s successful healthcare consolidation (CARE Hospitals, KIMS Health, $1 billion combined) and signals confidence in the K-12 infrastructure thesis.

Nord Anglia Education: International Entry

In February 2019, Canada Pension Plan Investment Board (CPPIB) and Baring Private Equity Asia–owned Nord Anglia Education acquired Oakridge International Schools for approximately ₹1,500–1,600 crore ($200 million). This cross-border transaction demonstrated appetite from global PE for Indian school assets and marked the first major entry of an international school brand into India through PE backing.

Cerestra Advisors: The Infrastructure Play

Cerestra pioneered the education infrastructure investment trust (Edu-Infra Fund) model. Rather than operating schools directly, Cerestra acquires the real estate assets of school chains and monetizes through infrastructure REITs. This sidesteps the legal non-profit restriction on schools themselves, enabling PE to realize returns through infrastructure appreciation and lease economics.

Cerestra later partnered with AnaCap Financial Partners to create a dedicated education infrastructure vehicle, acquiring Jain Group of Institutions’ K-12 and student housing assets—a blueprint now being adopted by other PE firms seeking to decouple real estate returns from operational compliance challenges.

PE-Backed School Chains: Detailed Snapshot

Sri Chaitanya Schools: The Troubled Consolidation

Sri Chaitanya represents both the opportunity and complexity of PE-backed K-12. Founded in 1986 by Dr. Bopanna Satyanarayana, the chain operates 750+ schools across 23 states with student fee collections exceeding ₹3,500 crore annually.

PE History

– 2010: New Silk Route invested $70 million for 33–49% stake—the largest foreign education investment at that time

– 2014: NSR attempted a $1+ billion exit as the investment cycle matured, but faced valuation disagreements with promoters

– 2019: Brookfield Asset Management and Kalpathi Investments expressed interest in a $1+ billion acquisition, but deals fell through

– 2021: NSR exited a 25% stake at ₹1,100 crore valuation (~$4 billion company valuation)

Lessons: While SR’s financial performance remained strong (EBITDA ~₹900 crore), the complexity of managing promoter expectations, regulatory scrutiny around non-profit mandates, and the difficulty of achieving exit valuations at desired multiples slowed consolidation. Sri Chaitanya’s inability to pursue an IPO (attempted twice with different partners) reflects the regulatory headwinds in India’s K-12 sector.

Narayana Schools: The Founder Buyback

Narayana Group, operating 750+ schools, represents a different exit narrative. Morgan Stanley and BanyanTree Capital invested $75 million in 2018, targeting a 5–7 year horizon. By 2023, the promoters (Ponguru Narayana’s family) decided to take full control, raising ₹1,150 crore via non-convertible debentures anchored by Barclays to provide a $160 million exit to the PE investors. The deal demonstrates how PE exits aren’t always trades to other investors; they can be founder recapitalization where promoters leverage the enhanced valuation and operational improvements driven by PE investment to regain control.

Gautam Adani & Sunny Varkey (GEMS Partnership)

In 2025, the Adani Foundation announced a ₹2,000 crore commitment to establish 20 schools over three years in partnership with GEMS Education, the Dubai-based K-12 giant. This 50-50 JV represents convergence of global capital, ESG commitment (30% seats free for underprivileged students), and asset-light consulting—GEMS will provide curriculum and training while Adani manages operations. This model addresses one of PE’s key pain points: how to scale without triggering non-profit restrictions.

Indus World Schools: The Failure Case Study

Career Launcher’s Indus World Schools (2005–2012) remains the cautionary tale for K-12 PE ventures in India. Founder Satya Narayanan ventured into K-12 schooling while operating a successful test-prep company. Despite HDFC’s ₹50 crore investment, the capital intensity, regulatory burden, and operational complexity of running physical schools contrasted sharply with the asset-light test-prep model. Indus World School of Business, the higher education arm, lost affiliation to Pondicherry University and suspended operations. The experience taught Narayanan a critical lesson: PE-backed education expansion works best when staying within a proven playbook. Career Launcher exited K-12 by 2011–12 to refocus on its core test-prep business, which later went public.

Mr Bhavin Shah, Director and CEO at EducationWorld, India’s largest read magazine addressing the education sector in India is a keen observer of the sector, he remarks that the rise of Private Equity in schools reflects confidence in education as a scalable, resilient sector. However, capital must remain a catalyst, not the compass. Growth, governance, and efficiency are welcome, but the core purpose of education, learning, character, and equity, must never be compromised in pursuit of returns.

Role of Impact Funds

While traditional PE seeks 25%+ IRRs, impact funds accept lower returns in exchange for social outcomes. Several are active in K-12:

- Acumen: Invests in affordable private schools and assessment solutions, with focus on learning outcomes and financial sustainability. Reports indicate Acumen’s K-12 sector strategy emphasizes schools serving lower-middle-income families.

- Omidyar Network: Supports innovative school models, teacher training, and education finance. Their portfolio includes Indian School Finance Co., demonstrating a blended approach to access and quality.

- Varthana: Pioneered education-focused non-bank lending, financing school infrastructure and teacher training. ChrysCapital led a $50 million series in 2018, validating the model of financing without ownership.

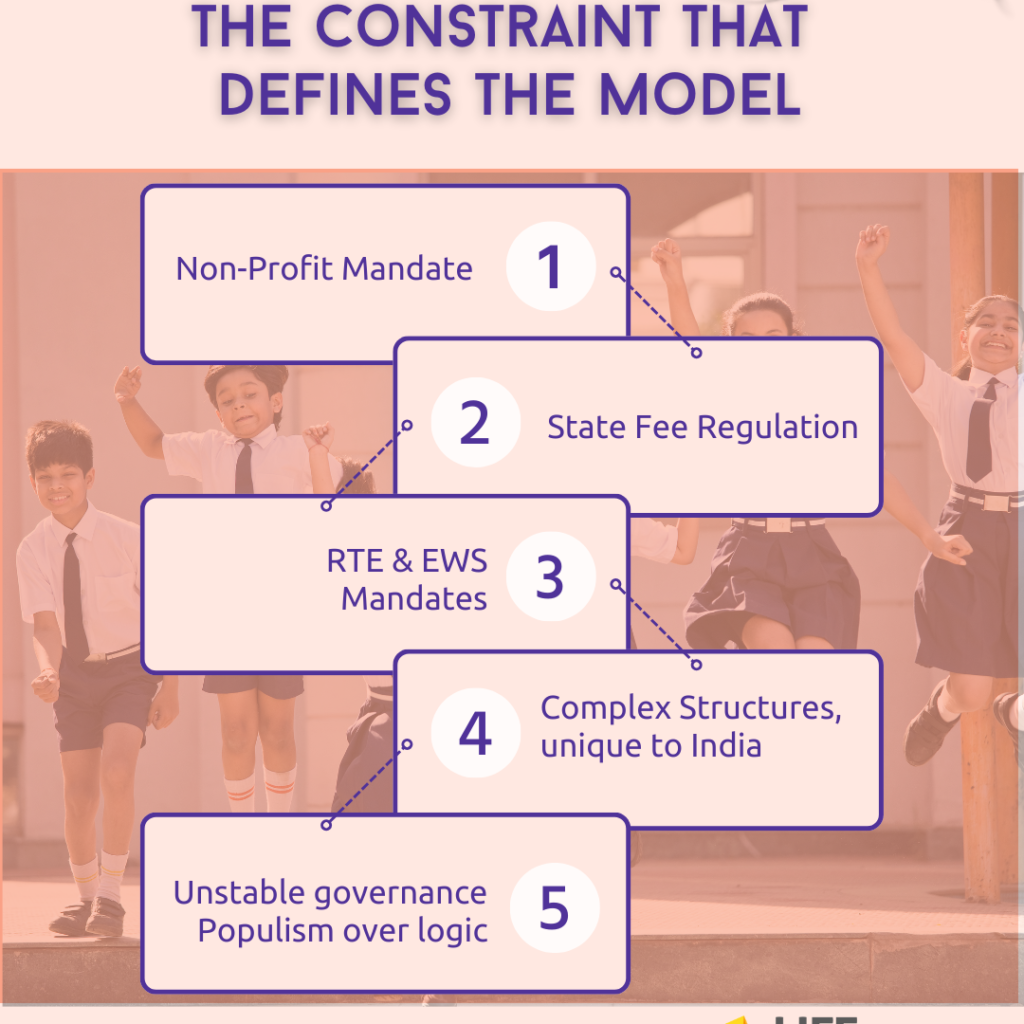

Challenges: The Constraint That Defines the Model

India’s constitutional and legal framework restricts K-12 schools from operating for profit. This architectural challenge shapes every PE investment thesis:

Key Constraints:

- Non-Profit Mandate (RTE Act 2009, Model Rules): Schools seeking recognition must declare they are “not run for profit to any individual, group or association.” Supreme Court verdicts (Unnikrishnan 1993, TMA Pai 2002) establish education as a “charity” and disallow profiteering, though “reasonable surplus” for expansion is permitted.

- Fee Regulation: No uniform national policy exists. States (Delhi, Karnataka, Maharashtra, Tamil Nadu, Gujarat, Rajasthan) impose fee caps ranging from 8–15% annual increases. Gujarat’s hard-cap model caps primary fees at ₹15,000 and secondary at ₹25,000, though exemptions for “Schools of Excellence” are contested.

- Right to Education / EWS Reservation: August 2024 Supreme Court ruling requires all private schools to reserve 25% seats for economically weaker students, reducing effective pricing power.

- Direct Restrictions: PE firms cannot directly own schools; they must operate through non-profit trusts or educational societies, necessitating complex structures where trusts own schools and PE firms provide services or own real estate.

- Unstable governance – Populism over logic: Education’s status as a state subject creates fragmented governance and policy unpredictability, often amplified by populist decisions that override academic and economic logic. This regulatory volatility raises risk premiums, disrupts long-term planning, and deters serious institutional investment in high-quality, scalable K–12 schools.

How PE Navigates These Restrictions

Service Company Model

K-12 Techno, Lighthouse, and Orchids operate through for-profit service entities that provide management, curriculum, technology, and staffing to schools registered as non-profits. PE owns the service company, not the school.

Infrastructure Play

Cerestra and AnaCap acquire the real estate underlying schools, monetizing through REIT structures that generate returns independent of school profitability restrictions.

Board Diversification

Lighthouse’s board includes education leaders (Indu Shahani) and business figures (Bijou Kurien, Ashish Kashyap) to ensure credibility and operational excellence beyond financial returns.

Why Multiples are Expanding

EdTech valuations have compressed to but offline K-12 schools with recurring tuition revenue and high operating leverage command premium multiples due to predictability and capital efficiency. The shift from high-growth, low-margin EdTech to profitable, scalable school operations explains PE appetite.

How to build an Investment Deck for K-12 Entrepreneurs

The PE Investment Lens in K-12

Every institutional investor evaluates K-12 through three simultaneous lenses

Lens 1: Education Outcomes (License to Operate)

- Learning outcomes

- Teacher quality & stability

- Parent trust / brand credibility

- Regulatory goodwill

Lens 2: Unit Economics (License to Scale)

- Contribution margin per student

- Teacher cost as % of revenue (ideal: <45%)

- Infrastructure ROI per seat

- Working capital advantage (advance fees)

Lens 3: Structuring Arbitrage (License to Monetize)

- ServiceCo vs Trust separation

- Infra monetization potential

- Exit optionality (secondary sale, REIT, founder recap)

Steps to follow

- Market Opportunity & Positioning

- Define addressable market (e.g., “4 million students in metros seeking international curricula” = ₹20,000 crore market at average ₹5 lakh tuition)

- Competitive Moat: Explain differentiation—branded portfolio, proprietary curriculum, teacher quality, technology integration, or geographic footprint

- Consolidation Play: Position as a platform that can acquire and absorb regional chains (as Lighthouse does)

- Unit Economics & Scalability

- Revenue per Student: Cost of tuition, average class size, infrastructure costs

- Contribution Margin: Tuition minus direct teacher costs (typically 60–70%)

- Operating Leverage: Show how EBITDA expands as you scale (demonstrated by K-12 Techno’s 21.7% margins)

- Working Capital: Tuition is collected upfront; highlight low cash conversion cycle

- Growth Trajectory & Traction

- Enrollment Growth: YoY student additions, retention rates, waitlist data

- Geographic Expansion: Footprint in 5+ cities reduces concentration risk

- Revenue Run Rate: FY24 revenue, FY25 YTD performance, visibility into next 12 months

- M&A Readiness: Can you absorb acquired schools into your operational template?

- Management & Governance

- Founder Track Record: Highlight education sector experience, prior exits, or operational turnarounds

- Board Composition: Include education leaders, business executives, and (if applicable) social sector figures

- Technology & Innovation: Showcase EdTech integrations (LMS, assessment platforms, ERP)

- Team Depth: Highlight functional leaders in curriculum, operations, finance, and technology

- Exit Visibility

- IPO Pathway: Reference CL Educate’s IPO, though acknowledge regulatory constraints and longer timelines vs. B2C tech

- Strategic Buyer Interest: Evidence of inbound interest from global chains (e.g., Nord Anglia, GEMS)

- Secondary Sale Potential: Show how PE can achieve 5–7 year exits to newer investors (Kenro Capital’s K-12 Techno deal, Venturi’s stake purchase)

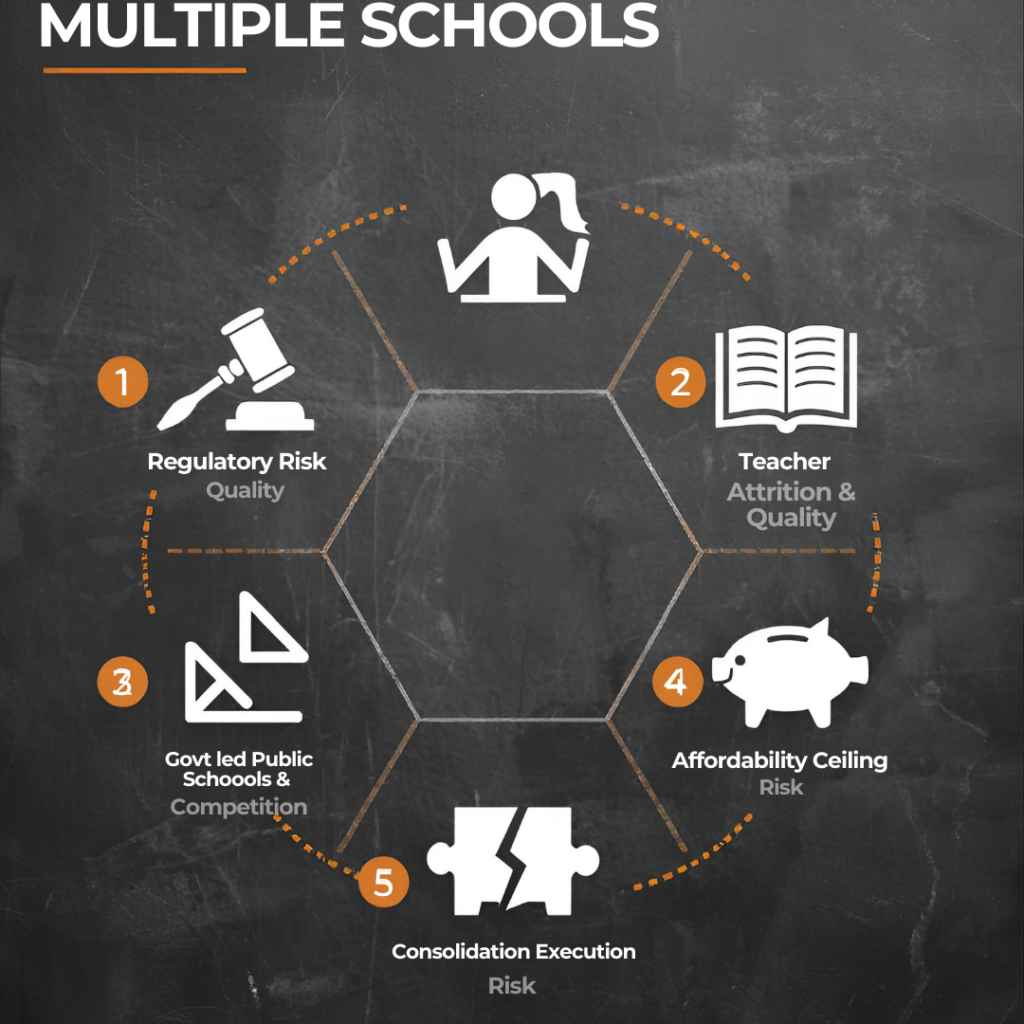

Challenges & Risks

- Regulatory Risk

- The RTE Act and fee regulation remain contentious. A hypothetical crackdown on “excessive” growth or compliance violations could impact valuation. Investors must assess state-level regulatory volatility—Tamil Nadu, Delhi, and Rajasthan are more active in enforcement than others.

- Teacher Attrition & Quality

- K-12 success depends on teacher quality, but India faces chronic shortages of trained educators. PE firms must invest in teacher training and retention, cutting into margins. Lighthouse’s emphasis on pedagogy training is a competitive response to this risk.

- Public School Competition

- Government spending on PM SHRI (Pradhan Mantri Schools for Rising India) and NEP 2020 implementation could strengthen public schools, dampening private school growth. Early investors in under-resourced geographies face execution risk.

- Affordability Ceiling

- Fee caps in almost all the states now, where a school is not allowed to increase beyond a certain single digit percentage every year. PE exits may be pressured if regulation tightens across major metros, eroding the high-margin expansion thesis.

- Consolidation Execution Risk

- Acquiring regional chains and integrating them into a standardized platform requires operational discipline. Cultural fit, technology migration, and teacher retention during integration are execution challenges that separate winners (Lighthouse) from strugglers.

Emerging Trends & Opportunities

Asset-Light Models Winning

K-12 Techno’s Eduvate platform, serving 800+ schools without owning them, is the fastest-growing segment. PE is rotating capital toward B2B SaaS models that avoid ownership headaches while scaling impact.

Infrastructure REITs as Exit Vehicles

Cerestra and AnaCap are pioneering education infrastructure investment trusts, allowing PE to monetize real estate separately from school operations. This may become a primary exit route given non-profit restrictions on schools themselves.

Global Capital Inflows

CPPIB (Oakridge), GEMS-Adani partnership, and KKR’s follow-on show sustained global capital interest. INR appreciation and India’s long-term growth narrative continue attracting sovereign wealth and pension funds.

The Inflection Point

India’s K-12 education sector stands at an inflection point. Consolidated platforms with recurring revenue, predictable unit economics, and clear operational templates are attracting institutional capital at scale. Entrepreneurs with differentiated brands, proven scalability, and regulatory clarity can access $50–200 million in PE funding within 3–5 years of demonstrating traction.

The non-profit constraint, far from being a fatal flaw, has forced PE to innovate—creating service company models, infrastructure plays, and B2B platforms that are often more sustainable than traditional ownership. Investors should focus on management quality, regulatory positioning, and path to profitability rather than hyper-growth narratives that dominated EdTech.

Abhiney Singh, Partner at LIFE Educare and promoter of a CBSE school with 3,000+ students, notes that the volume of organised and unorganised players looking to enter the K–12 sector today is nothing short of staggering. At LIFE Educare, we now receive close to two enquiries every month from promoters seeking structured business plans to launch school ventures. What’s striking is the common thread across these conversations—a clear intent to build centralised academic and operational teams, rather than fragmented, owner-led models. Over the next decade, full-stack school operations—everything except brick-and-mortar construction—are likely to evolve into a large, scalable business in themselves. The future of K–12 may well belong to those who can separate school ownership from school excellence.

For aspiring entrepreneurs, the playbook is clear: build a strong unit economics foundation, demonstrate geographic replicability, and prepare for disciplined M&A execution. PE backing is no longer a luxury; it’s an essential ingredient for scaling K-12 platforms in India’s fragmented but dynamic market.